Disruption is inevitable: We are prepared

We at Ambit are constantly trying to stay ahead of the curve by drowning out the noise and looking ahead. In keeping with our long term investment thesis, we like to stay up to date with not just the present impediments faced by your portfolio companies but also long term disruptions which can hit these companies. Hence we will regularly come out with our thoughts on disruptions in your portfolio companies/ sectors and for the 20th volume of this series we have selected Garware Technical Fibres. This note takes a closer look at challenges facing Garware Technical Fibres how the company is placed to tackle those.

Garware Technical Fibres Limited

Garware Technical Fibres (GTFL) (Formerly Garware Wall Ropes) – established in 1976 – is one of India’s leading players in the technical textiles sector. The company has evolved to a great extent over the last 4 decades –

- 1976 – 1990 – Focus on Commoditized Products: Established in 1976, the company’s focus was on commoditized products such as ropes and twines addressing the fisheries and allied sectors.

- 1990 – 2011 – Diversifying end user industry: Over the next two decades, GTFL improved its product portfolio by upgrading existing portfolio with a higher number of SKU’s while also addressing other industries with similar applications such as sports and agriculture during the period.

- Post 2011 – Passing on the baton: The bulk of transformation can be attributed to when Vayu Garware took over as CMD in 2011. Vayu Garware brought a slew of changes which transformed the organization into a multi-divisional, multi-geographical technical textiles company with presence in over 75 countries.

The major changes undertaken by Vayu Garware were –

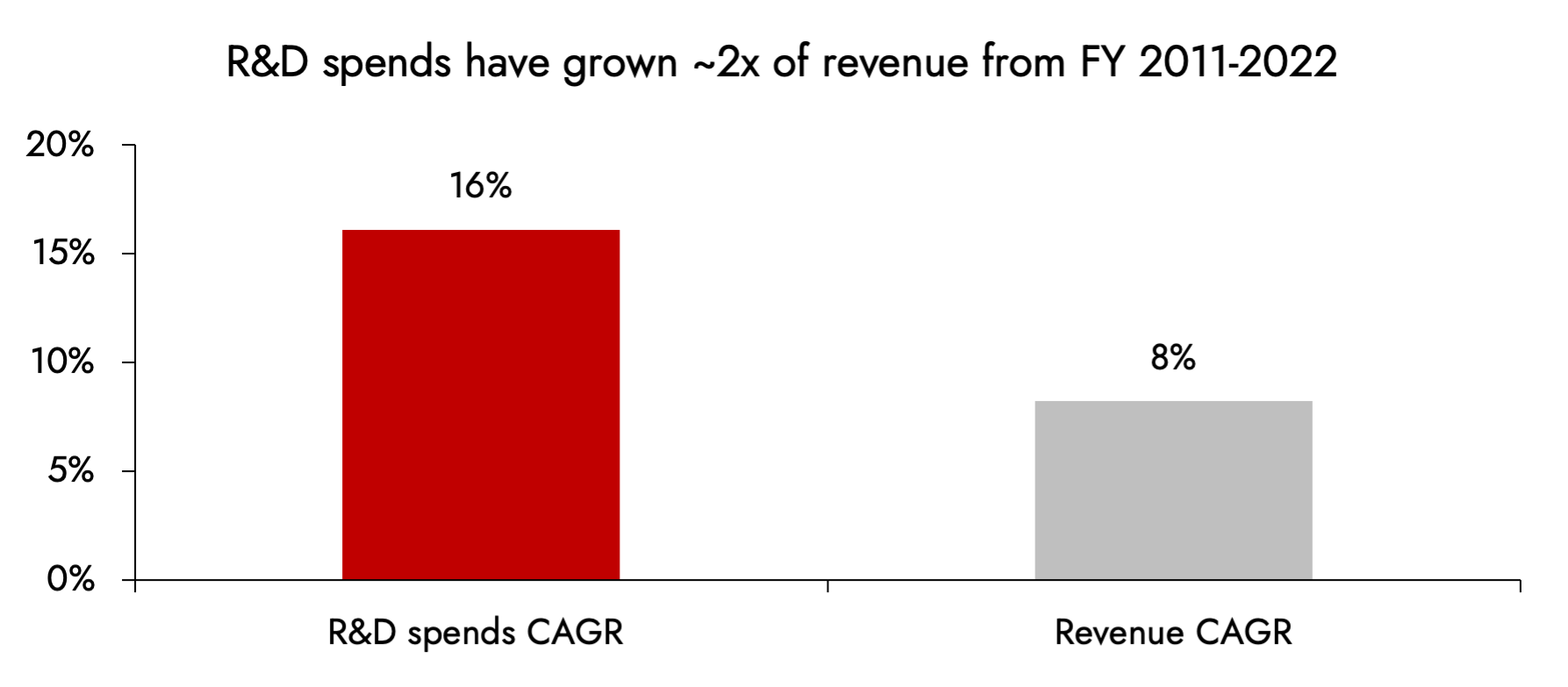

1. Focus on Innovation – Post 2011, GTFL started investing heavily in Research and Development in order to transform into a more value added focused business. R&D spends have increased by ~6X from Rs1.9Cr in FY11 to Rs9.7Cr in FY22 (Refer Exhibit 1) which has resulted in profitability far outpacing top-line growth for the company. (Refer Exhibit 2).

This increased focus on R&D has resulted in GTFL filing 75 patents and being granted 23 patents as on FY22. Moreover, the ability to innovate and to address problems faced by the client has helped Garware one of the preferred suppliers to clients, in addition to expanding the addressable market size and shortening product life cycle.

Exhibit 1: R&D spends have grown at a CAGR of 16% since FY 2011 post Vayu Garware being elevated as MD

Source: Ambit Asset Management

2. Professionalizing set-up – Vayu Garware brought in Shujaul Rehman as COO and President in 2012. Shujaul Rehman has since taken over the role of CEO and is now managing a team of 8 functional heads.

GTFL has also hired professionals such as Alex Sutherland as the head of its Scotland operations. He was the ex-MD of Marine Harvest (now Mowi) for ~9 years. Mowi is the largest producer of Atlantic salmon in the world and one of the key clients for GTFL in the aquaculture segment.

In addition to bringing external professionals such as Shujaul Rehman and Alex Sutherland, GTFL has also adopted the business philosophies of Kaizen, Total Process Management, 5S Framework, Kanban, 8D Process, Advanced Product Quality Planning, Pull System and Jishu Hozen to drive excellence on the manufacturing front.

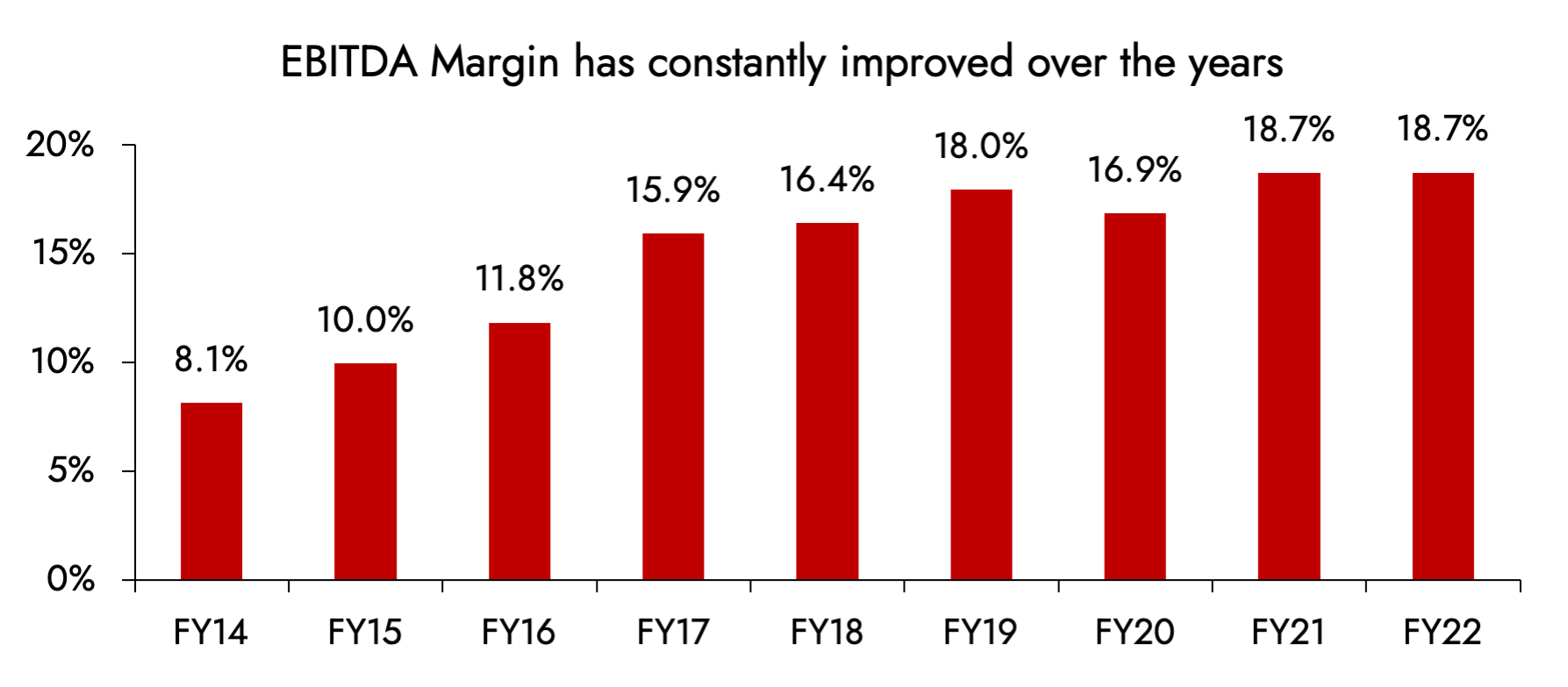

Adoption and execution of the above strategies can be seen on GTFL’s shop-floor with the focus on continuous improvement and incentives given across the board for suggestions provided by workforce which have resulted in efficiencies coming on board (Refer Exhibit 2).

Exhibit 2: Professionalizing set-up and increase in value added mix has resulted in substantial margin improvement

Source: Ambit Asset Management, Company

3. Premiumization + solution oriented company – The focus on innovation and striving for continued improvement has resulted in gradually increasing mix from value added products which now >75% of the company’s revenue, which is a stark contrast to its primarily commoditized portfolio pre 2011.

In addition to the same, focus on being a solution oriented company and working in collaboration with clients has resulted in high contribution of new products (launched over the past 3 years) which stands at ~30%/40% of Sales/ PAT.

Using these innovations, Garware has been able to tackle the major problems of salmon fishing companies such as bio-fouling and tuna attacks on salmon farms by introducing V2 and Sapphire CFR. (Refer Exhibit 3)

Exhibit 3: Garware’s ability to innovate and provide solution-oriented value-added products is amongst the strongest globally

Source: Ambit Asset Management, Company

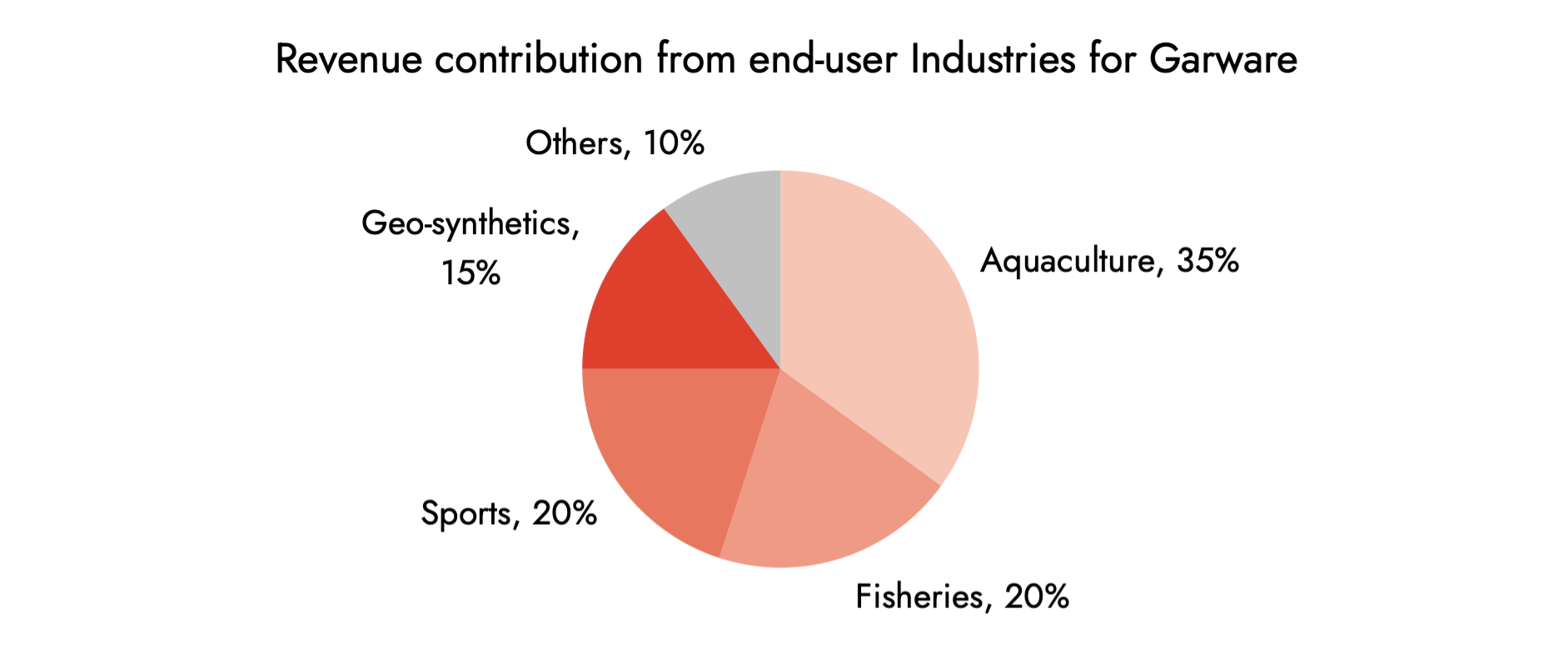

GTFL has successfully leveraged these innovations to provide solutions to many domestic industries such as – fisheries, sports, aqua-culture, geo-synthetics, agriculture and industrials – thus helping it withstand the cyclical nature of the industry. Focus on premiumization, value and solution-oriented products has resulted in continuous margin improvement for the company.

Scanning for Disruptions –

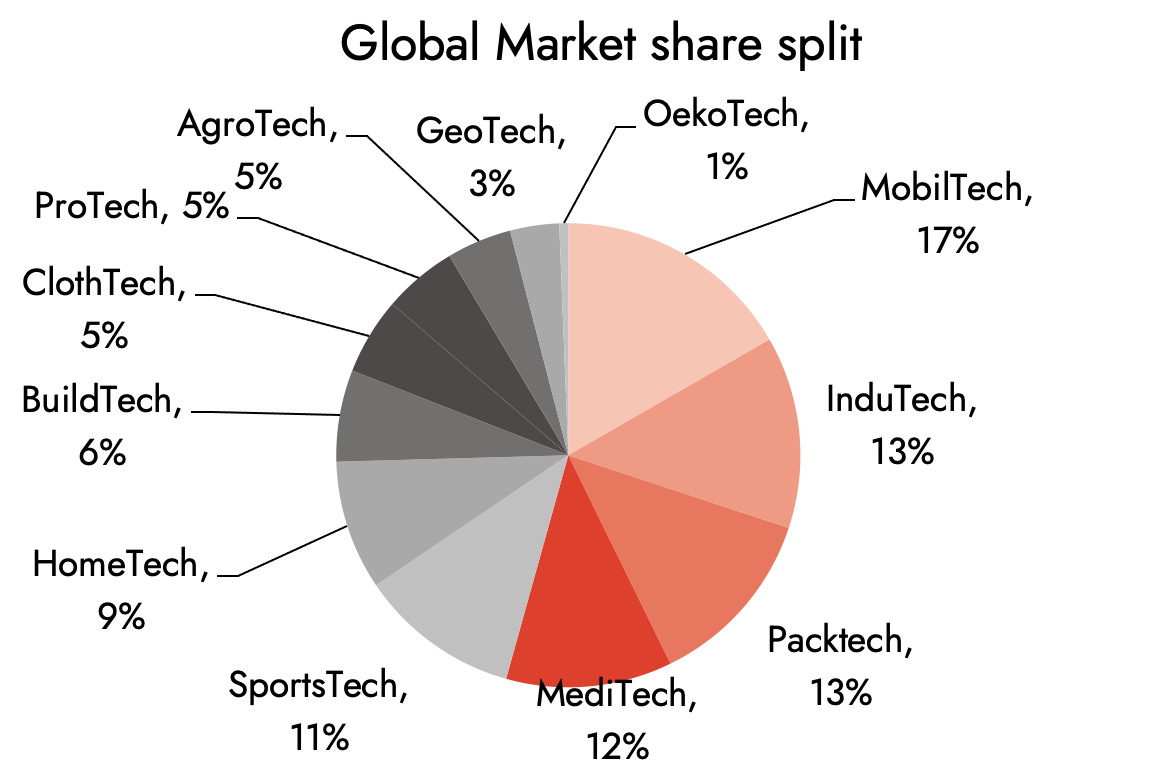

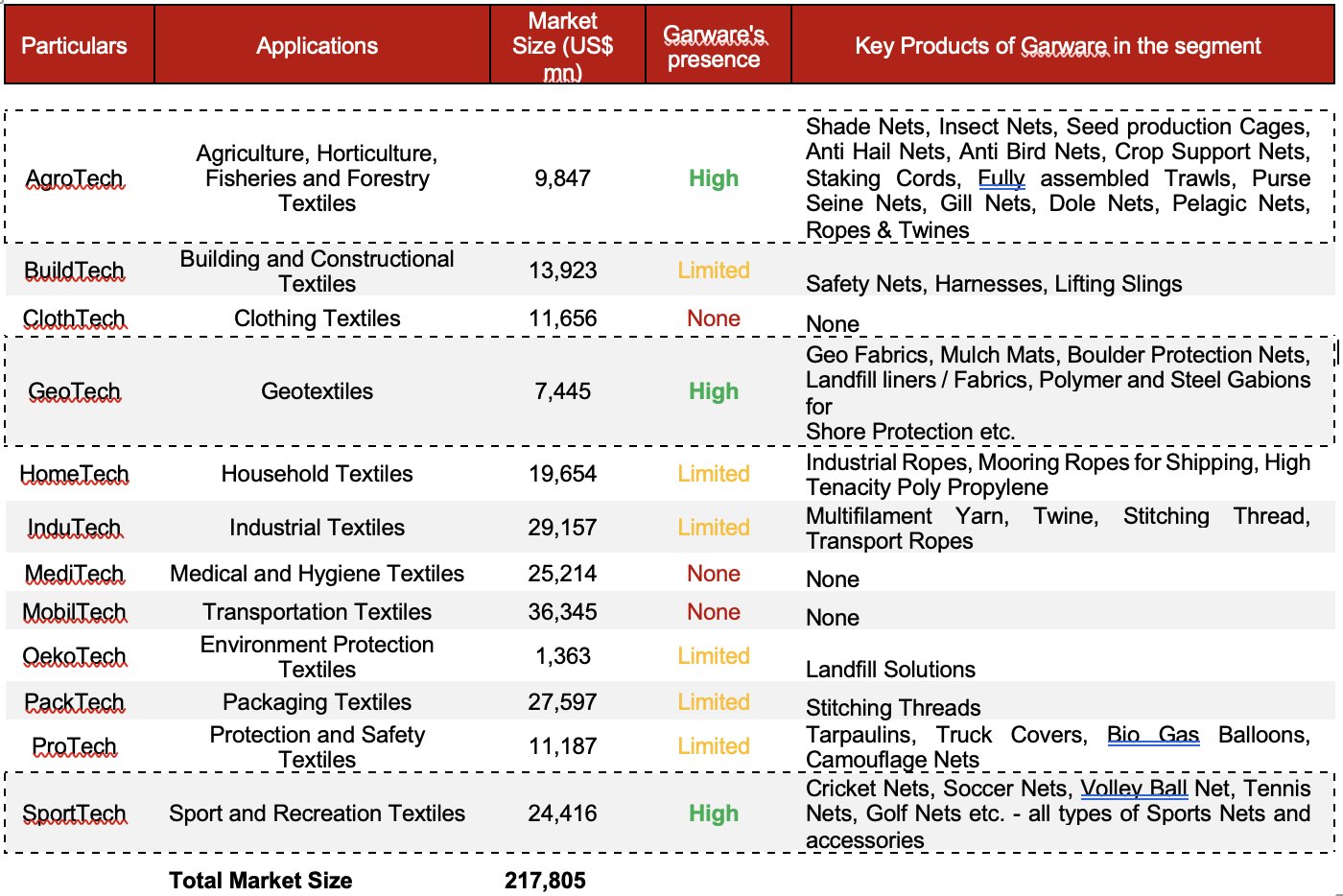

1. Competitive Intensity – Technical Textiles is estimated to be ~218 billion USD market, While Indian technical fibres is a ~19 billion USD market. This industry can be broadly divided into 12 segments which are Agrotech, buildtech, clothtech, geotech, household tech, industrial tech, meditech, mobiltech, oekotech, packtech, protech and Sporttech respectively. (Refer exhibits 4 and 5)

Exhibit 4: Global market for technical fibres is ~USD218bn led by MobilTech

Source: Ambit Asset Management, Technical Texile Industry Baseline study, 2020

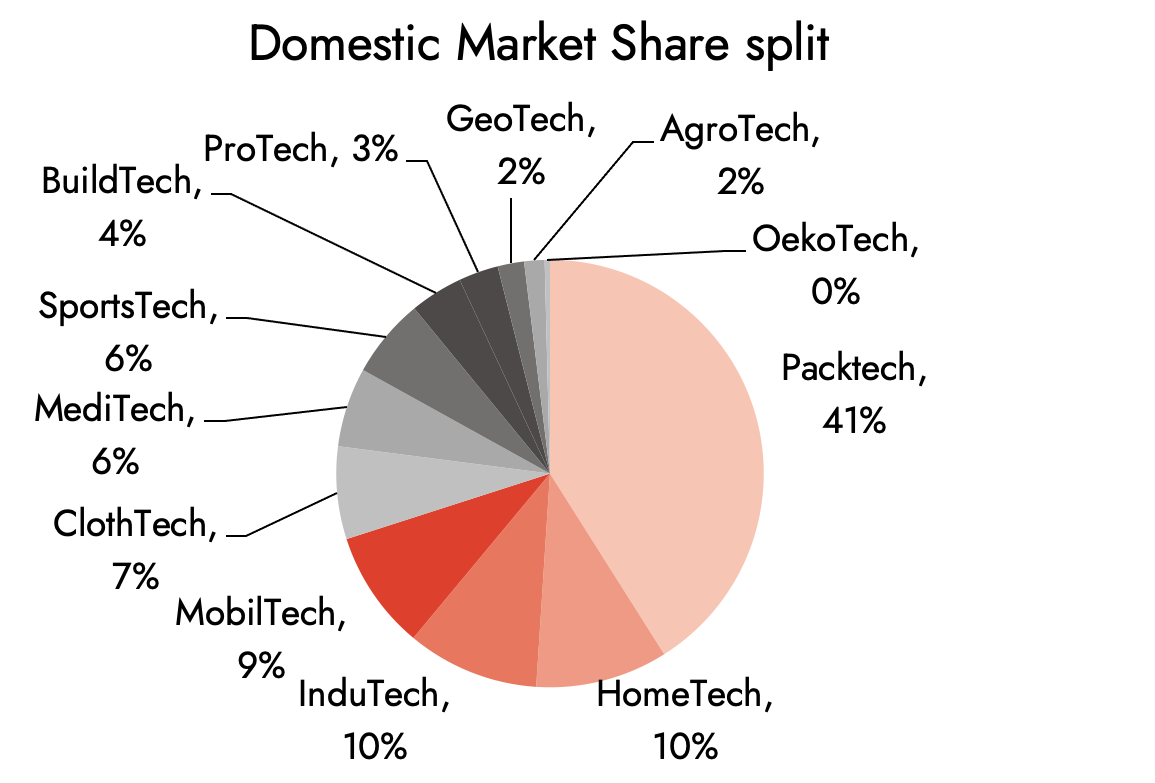

Exhibit 5: …whereas Indian market is <10% of global market with PackTech having a massive share

Source: Ambit Asset Management, Technical Texile Industry Baseline study, 2020

While the market opportunity remains large, Garware’s focus areas are limited to a few sub-segments such as AgroTech, SportTech and GeoTech.( Refer Exhibit 6 &7)

Exhibit 6: GTFL ‘s contribution from end-user segments

Source: Ambit Asset Management Estimates. Actuals may differ slightly

Exhibit 7: GTFL presence is still very limited to 3 sub-segments

Source: Ambit Asset Management, Technical Texile Industry Baseline study, 2020. Dotted lines indicate higher priority for GTFL

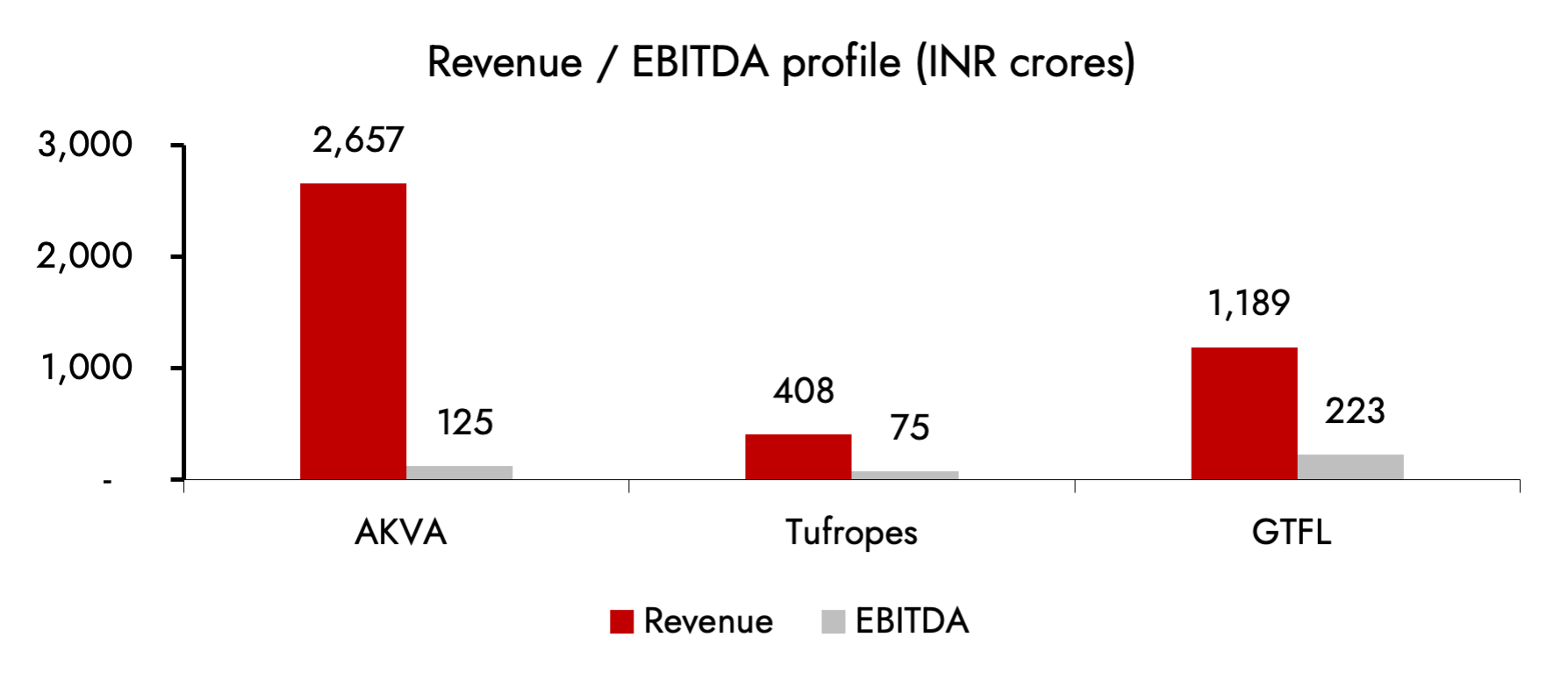

GTFL is a market leader in domestic fisheries and aquaculture sub-segment globally however it faces competition from Tufropes in this sub-segment domestically and with AKVA on the salmon fishing side. Any substantial increase on the competition front may impact GTFL.

AKVA, headquartered in Norway, is a supplier for solutions and services to the aqua-culture industry primarily catering to salmon (~80% of revenues). The company provides solutions in marine infrastructure such as nets, anchoring and mooring and plastic pens along with digital and land based fish farming solutions. There is a reasonable overlap of AKVA’s products with GTFL on the marine infrastructure front. AKVA’s FY22 revenue of ~Rs2,657 crores was >2x of GTFL’s revenues, albeit at a lower profitability. Despite a larger scale and size, AKVA’s growth (~2%) has been substantially weaker to GTFL, implying market share loss.

Mumbai based Tufropes Pvt. Ltd., is a manufacturer of synthetic ropes and nets which deals in marine and shipping, aquaculture, agriculture, sports, industrial and commercial applications which has a major overlap with GTFL’s portfolio. Tufropes’ FY21 Revenue/EBITDA of Rs408Cr/Rs75Cr was ~1/3rd of GTFL.

Exhibit 8: GTFL’s share of profit pool is higher than its direct competitors

Source: Ambit Asset Management, company, CARE Rating. For AKVA, Revenue is for C.Y. 2022, NOK is exchanged at a rate of 7.87 as on 3rd March, 2023.For Tufropes revenue and EBITDA are for FY21

Despite such a massive domestic and international market GTFL is still just a marginal player, even in areas where it has ample opportunities to diversify and capture incremental market share. GTFL while having a healthy presence on salmon fishing front it is now looking to cater to other species such as Barramundi, Sea Bass, Sea Bream, Amberjack and Tilapia.

While the competitive intensity exists in the sector, we anticipate GTFL to continue market share gains in core and adjacent segment owing to R&D focused approach, track record of acquisition and deepening relationships with marquee clients.

2. Challenges impacting end-user segments – Key areas for GTFL are aquaculture (primarily salmon farming), sports and fisheries (~ >2/3rd of total revenues) while key geographies being Norway, Chile and Scotland for salmon farming; USA and Europe for sports nets; and India primarily for fisheries. Any potential regulation that may impact the end-user industry in these geographies could be a major disruption for GTFL.

For Eg. In Norway, which accounts for more than half of global salmon fishing, a key market for GTFL, the Norwegian government in September 2022 announced a 40% tax called ground rent tax starting January 2023 which effectively increases tax rate for salmon farmers (a key clientele for GTFL) from 22% to 62% and as high as 80% including Norwegian wealth tax. The above proposition will be put to a parliamentary vote which is expected to be in either March or April 2023. Following this, majority of the large salmon farmers have halted future capex which may indirectly impact GTFL.

Further any slowdown in other segments may impact demand for GTFL going ahead

However, GTFL should be relatively well insulated to such external shocks primarily due to a well-diversified portfolio with over ~20,000 SKU’s and catering to multiple end-user categories. Also, GTFL products, while critical to the performance of end-user segments, constitute an insignificant portion of the costs for the enterprises (For eg: Fishing nets are only ~5% of total costs for a fishing company). The relative important nature of the business along with increasing use cases and applications makes GTFL relatively well placed to absorb any potential disruptions in some segments or geographies.

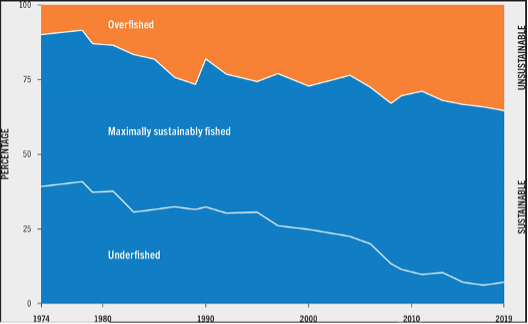

3. Environmental challenges – >50% of revenues for GTFL comes from fishing or ancillary activities. Overfishing remains one of the key concerns for the industry. Global consumption of aquatic foods has increased at an average annual rate of 3.0 % since 1961, compared with a population growth rate of 1.6%. On a per capita basis, consumption of aquatic food grew from an average of 9.9 kg in the 1960s to 20.2 kg in 2020. Increase in overfishing: the share of overfished marine fisheries stocks is increasing sharply presenting ecological and environmental concerns.

Exhibit 9: World’s marine fisheries stocks indicates overfishing as a key concern area and is only getting worse

Source: Ambit Asset Management, Food and Agricultural Organization of UN

Climate concern: In addition to the same, climate change impact on oceans and waterbodies have seen changes in migration patterns of some fish which can have long lasting economic impact to the industry.

Government restrictions: The fisheries department in India has also announced several bans on fishing. In 2022, the fisheries department announced an annual fishing ban for 61 days from April 15 to June 14 for the east coast and from 1stJune to 31st July, 2022 for the west coast in for conservation and effective management of fishery resources.

Any major extended bans on fishing along with potential global climate related challenges may result in probable disruptions for companies such as GTFL.

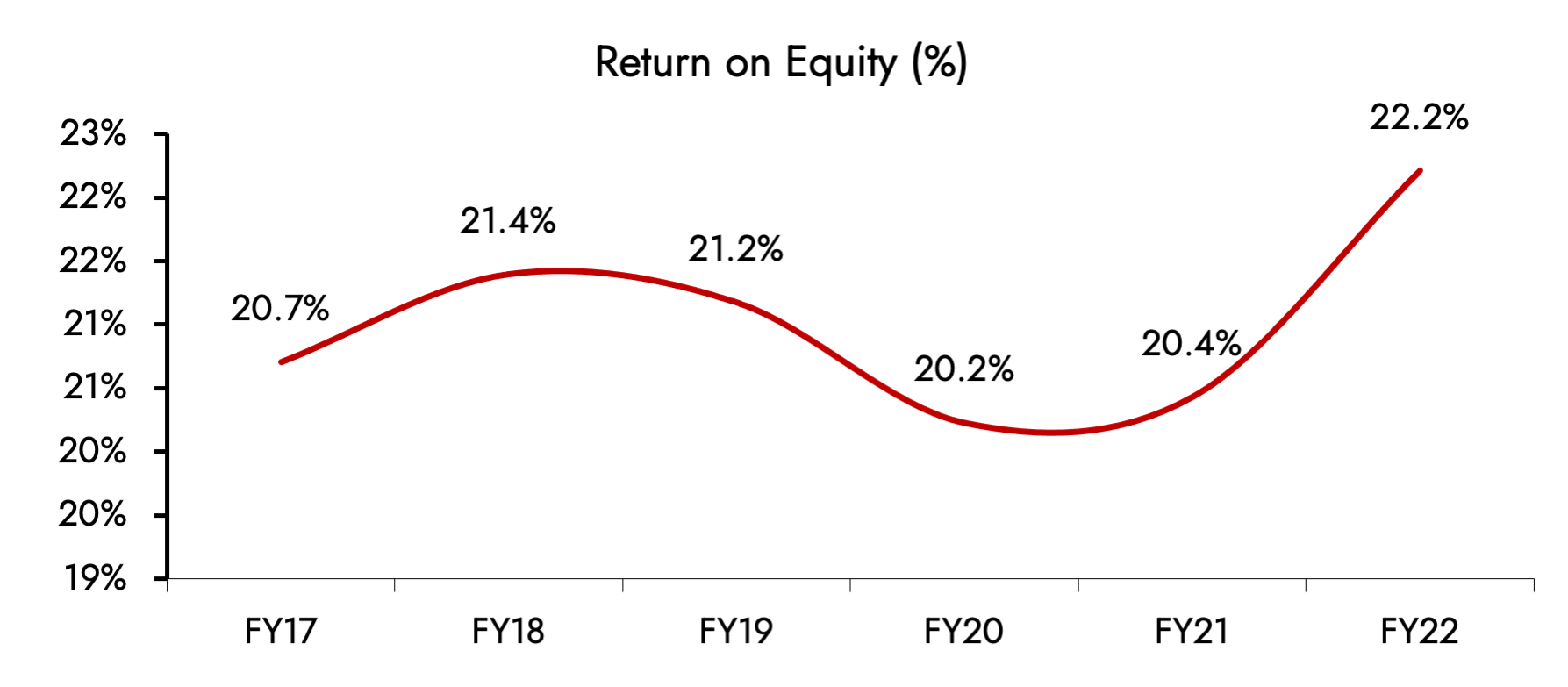

4. Capital Misallocation – Garware Technical Fibres as a company over the past few years has been prudent in capital allocation resulting in a net cash position of ~Rs550 crores as on September 2022. With the company’s current manufacturing plants in Wai and Pune, focus on R&D and sufficient capacities already in place the company is unlikely to require substantial capital from this cash pool for growth.

Exhibit 10 : Garware’s return profile has remained robust despite multiple disruptions

Source: Ambit Asset Management, Company

Garware’s probable use of cash in books can either be utilized in higher paybacks to existing shareholders or for inorganic forays. Any inorganic foray which is value dilutive to existing shareholders, such as –

- Limited or no synergies to existing business

- Overpaying for an acquisition

- Acquisition of an entity with inferior return profile (and inability to turnaround) resulting in dilution of GTFL’s overall return profile,

May result in potential disruption for GTFL. While currently, there haven’t been any instances of capital misallocation on GTFL’s part, misuse of cash remains a key disruption risk.

5. External risks related to input and other costs – GTFL’s key input costs are HDPE (High Density Polyethylene) and Polypropylene which are crude derivatives. With the current uncertain global environment we have seen massive fluctuations in crude and crude derivatives (Refer Exhibit 11). Any sharp volatility in prices of the crude derivatives directly impacts the company’s gross margins. Moreover, demand - supply mismatch in shipping industry has resulted in sharp volatility in shipping rates, which may impact margins as exports form a majority of the revenue (Refer Exhibit 12). Any macro-global disruption may result in impact on profitability for GTFL.

6. Redundancy of GTFL’s products –

a. Superior Product – In the past, GTFL’s products – such as HDPE nets – have been able to garner substantial market share from products made of Nylon, primarily because of better functionalities. While Nylon may be strong in drier areas, it is hydrophilic under water which results in weakening of the material over time. However, Garware’s HDPE nets are hydrophobic under water which results in a longer useful life of GTFL’s nets. Any potential solutions which are better than GTFL’s products may result in probable disruptions. However, currently there have been no indication of the same and GTFL remains one of the preferred players in the segments it operates in.

b. Product obsolescence – Fishing nets have been in practice for over 10,000 years, however recent developments may impact the saliance of fishing. Land farming is a concept where microbial conditions and chemistry of water is replicated in land farms away from coastlines. Proximar Seafood – A land based salmon farming company – claims to achieve high quality production and stable harvest volumes all-year round, with minimal use of water, electricity and additives.

c. The ability to mimic nature artificially is extremely difficult, which, along with high energy cost have resulted in land based farming not being commercially successful. If Land based salmon farming becomes successful, it may result in several disruptions and may impact the use of technical fibres in the industry.

Based on the above, we currently anticipate minimal risks of obsolescence and superior product. However any indication of any change may result in disruption.

Conclusion

Garware Technical Fibres stands out as one of the few Indian enterprises driving game-changing innovation in technical textiles on a global scale. Garware’s track record, which includes working in-collaboration with clients and delivering innovative solutions are just a glimpse of the ability of GTFL to be a reliable partner for large organizations. This also sets up a strong back-bone for the company to use its expertise in both existing and newer areas. While there are several short term disruptions which may impact the company, the company has all the ingredients to address the huge addressable market size.